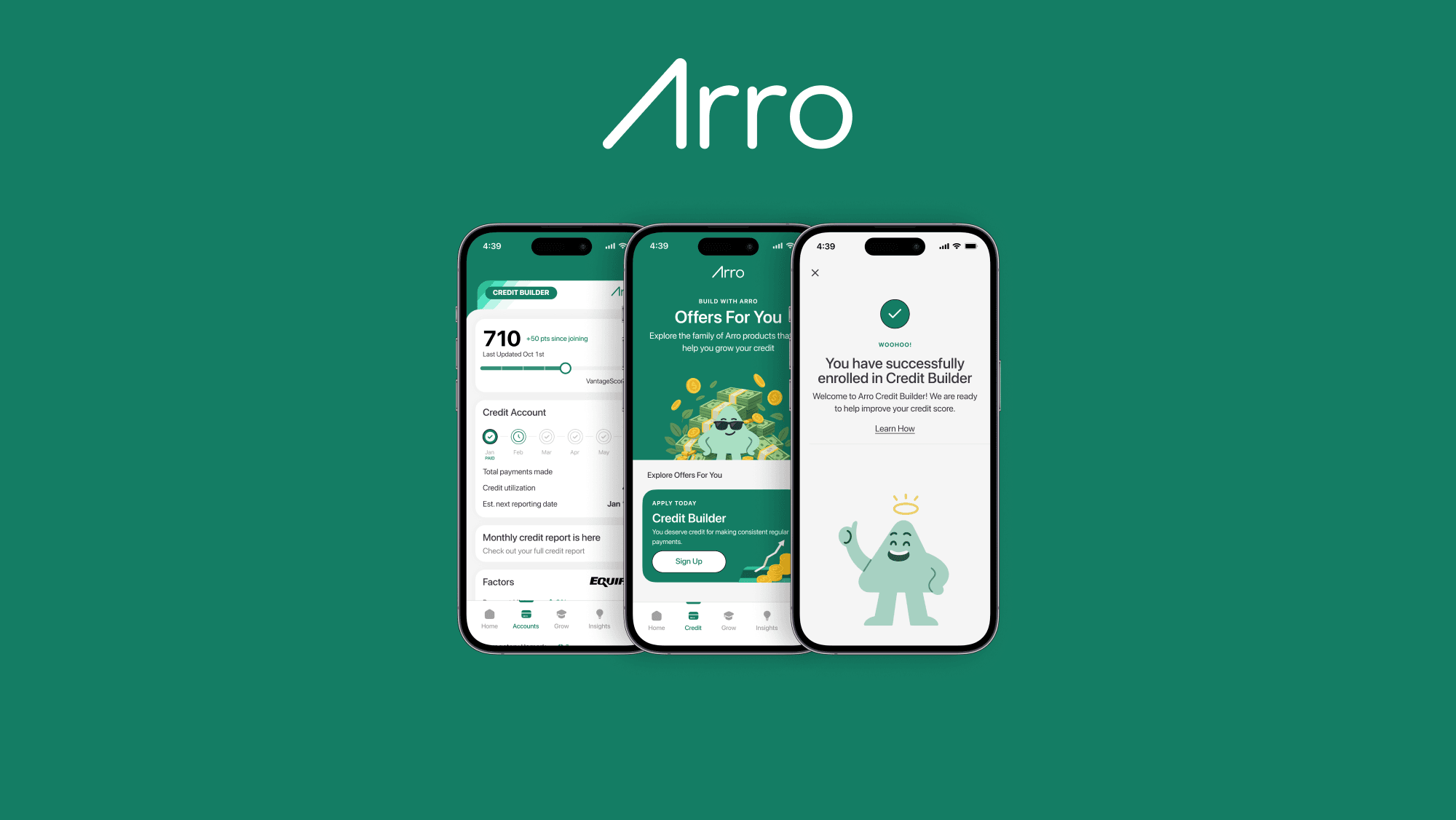

The Arro Credit Builder is one of the simpler credit-building products on the market. You pay $12 a month, Arro reports a $2,000 tradeline to all three major credit bureaus, and that positive payment history shows up on your credit report. No deposit, no security check, no waiting to qualify.

Is it worth $144 a year? It depends on what you would otherwise pay to build credit, and how Arro's structure compares to Self.Inc Credit Builder Account, Kikoff, and other established options. Here is the full breakdown.

Arro Credit Builder at a glance

Cost: $12 per month, $144 per year.

Reported tradeline: $2,000, classified as an installment account.

Reports to: Experian, Equifax, TransUnion.

Term length: Ongoing, month to month. Cancel anytime.

Hard credit pull at signup: No. Approval does not affect your credit — see how soft pull pre-approval works for context.

Best for: People with thin or no credit history who want a quick, no-deposit way to add a positive installment tradeline to their credit report.

How the Arro Credit Builder actually works

Unlike a traditional credit-builder loan, Arro is not really lending you money. It is reporting a tradeline that looks like an installment loan, while you pay a monthly subscription fee for the service.

Each month you pay $12. Arro reports your account as current and in good standing. Over time, that consistent positive payment history shows up as a steady installment account on your credit report, which improves your credit mix and adds to your average account age.

Arro Credit Builder

Arro Credit Builder

Arro is your financial growth partner. Start with Credit Builder — a $2,000 tradeline reported to major bureaus for just $12/month.

Standout feature

No credit check, no security deposit

Fees

$12/month ($0.99 first month) or $96/year

Pros

You're not borrowing — no debt or interest to manage

Cons

Does not report to TransUnion

What this does to your credit score

Three credit score factors get a boost.

Payment history (35% of FICO). Every on-time monthly payment to Arro adds a positive mark. Over 6 to 12 months, this is the single biggest score lever. (For the flip-side of how payment behavior can hurt you, see does paying minimum balance hurt credit score.)

Credit mix (10% of FICO). If you only have credit cards on your report, adding an installment account diversifies the mix, which often nudges the score upward.

Average age of accounts (15% of FICO). Once the Arro tradeline is open, it ages on your report. The longer you keep it, the more it helps.

Most users see 20 to 60 points of score movement within 3 to 6 months of starting, depending on the rest of their credit profile. Thin files see bigger gains because there is less existing data to dilute the new positive activity. If you are starting from scratch, our guide to credit building in your 20s walks through the broader playbook.

What it costs over time

$12 a month is $144 a year. Over two years, that is $288. Compare that to alternatives:

- Self.Inc Credit Builder Account: Plans start at around $25 a month, but the deposits come back to you at the end of the term as savings. Net cost is just the administrative fees, usually $9 to $15.

- Kikoff Credit Account: $5 a month for a $750 reported tradeline. Cheaper, but a smaller reported account size.

- Cheers Credit Builder Loan: No subscription fee, AI-powered, structured more like a traditional builder loan.

If the only metric is dollars-per-credit-month, Kikoff is cheaper. If you want a higher reported balance for credit mix and age, Arro's $2,000 tradeline is larger. The Self.Inc Credit Builder Account doubles as forced savings, which means your net cost is dramatically lower if you actually keep the deposits.

What Arro Credit Builder does well

No deposit required. Many credit-builder loans want $25 to $50 a month locked into savings. Arro skips that.

No credit check at signup. Anyone can sign up, regardless of credit score or thin file.

Reports to all three bureaus. Some smaller builders only report to one or two, which limits how widely the score boost spreads.

Month-to-month flexibility. Cancel anytime without penalty. Most builder loans lock you into a 12 or 24 month term.

What to watch out for

You are paying for the service. Unlike a true builder loan, the money you pay each month does not become your savings. It is a fee for the credit reporting, full stop.

The credit gain is gradual. Like every credit-builder product, the score lift comes from consistent monthly reporting, not from a single payment. Plan for 3 to 6 months minimum to see meaningful movement.

The tradeline shows as a finance account, not a major bank or credit card. Lenders see it on your report, but it does not carry as much weight as a major-bank credit card or auto loan.

Does not replace a credit card. To diversify into both installment and revolving credit, pair the Arro Credit Builder with a credit card. The Self Visa® Credit Card and the Arro Card itself are reasonable options — keeping revolving utilization low on whatever card you pick is what actually moves the score.

Pair it with a revolving card

Since the Arro tradeline only covers the installment side of your file, a secured card rounds out the revolving half. The Self Visa is a clean way to add that revolving line, and the Self Visa reports to all three bureaus just like Arro does, so on-time activity on both accounts compounds your payment history faster than either one alone.

Who should consider the Arro Credit Builder

Four profiles where it fits.

You have thin credit (fewer than 3 active tradelines) and want to add an installment account quickly.

You cannot or do not want to lock up $200 to $500 in a refundable deposit.

You want a hands-off, fee-based service rather than a structured loan.

You plan to use Arro for 6 to 12 months as part of a broader credit-building plan.

If you see yourself in those profiles, the Arro Credit Builder is an easy way to get a $2,000 installment tradeline reporting fast, and Arro keeps it month to month so you stay in control of the cost.

Arro Credit Builder

Arro Credit Builder

Arro is your financial growth partner. Start with Credit Builder — a $2,000 tradeline reported to major bureaus for just $12/month.

Standout feature

No credit check, no security deposit

Fees

$12/month ($0.99 first month) or $96/year

Pros

You're not borrowing — no debt or interest to manage

Cons

Does not report to TransUnion

Who should look elsewhere

If you want your monthly payments to also be savings, the Self.Inc Credit Builder Account is more cost-effective because the deposits come back to you. If you want the cheapest reported tradeline period, Kikoff at $5 a month is the budget pick. If your credit is already healthy and you mainly want to clean up errors, Dovly's free AI credit engine and Creditship credit monitoring are better next steps than another tradeline.

Frequently Asked Questions

Does the Arro Credit Builder really build my credit?

Yes, when used consistently. Arro reports a $2,000 installment-style tradeline to all three credit bureaus each month. On-time payments add positive payment history, which is 35% of your FICO score. Most users see meaningful score gains within 3 to 6 months, especially if they have thin credit files.

How is Arro different from a traditional credit-builder loan?

In a traditional credit-builder loan like the Self.Inc Credit Builder Account, you make monthly payments that go into a locked savings account, and you get the money back at the end of the term. Arro is structured as a monthly subscription fee, so your $12 a month is a service charge rather than savings. It is simpler but does not double as a savings tool.

Will signing up for Arro hurt my credit?

No. Arro does not pull a hard inquiry at signup, so the application itself does not affect your credit score. Once the account opens and starts reporting, the new tradeline can briefly lower your average age of accounts, but the positive monthly reporting typically more than offsets that within a few months.

Can I cancel the Arro Credit Builder anytime?

Yes. The Arro Credit Builder is month-to-month with no long-term contract. You can cancel anytime through the app without penalty. The tradeline remains on your credit report for several years after closing, which means it continues to age and contribute to your average account age.