Easiest Unsecured Credit Cards to Get Approved For

Understanding Unsecured Credit Cards

An unsecured credit card extends a line of credit without requiring collateral like a cash deposit. Most unsecured cards check your credit history and income before approval. For people with little or poor credit history, the easiest unsecured credit card to get tend to include cards designed by fintech companies such as Perpay, Zolve, Atlas, Possible, and Self.

How to Choose an Unsecured Credit Card for Bad Credit

When choosing the easiest unsecured credit card to get, consider these factors:

- Approval Criteria: Some cards accept limited credit profiles or alternative data (income, bank transaction history) rather than strict credit scores.

- Fees: Look for annual or monthly fees and compare them against expected rewards or credit-building benefits.

- APR. APR is one of the most important factors to review. Many unsecured cards for bad credit carry higher interest rates because lenders take on more risk without a security deposit. Variable APRs for bad credit unsecured cards often range between 25% and 36%, depending on the issuer and your profile.

- Credit Reporting: Ensure the card reports your activity to at least two or three major credit bureaus, so on-time payments help your score growth.

- Rewards and Perks: Some cards include cash back or perks even if they are designed for credit building.

- Credit Limit and Upgrade Path. Some issuers increase your credit limit after several months of on-time payments. A higher limit can help lower your utilization ratio and improve your score over time.

How to Build Your Credit With An Unsecured Credit Card

Getting approved for the easiest unsecured credit card to get is only the first step. The real impact on your credit score comes from how you use the card after approval. A credit card can help you build strong credit if you use it strategically and consistently.

Below are the most important factors that influence your score and how to manage them.

1. Pay On Time Every Month

Payment history makes up the largest portion of your credit score. One late payment can significantly lower your score and stay on your credit report for up to seven years.

Set up autopay for at least the minimum payment. Ideally, pay the full statement balance before the due date. If you use the easiest unsecured credit card to get but miss payments, it can hurt your credit instead of helping it.

2. Keep Your Credit Utilization Low

Credit utilization refers to how much of your available credit you use. For example, if your credit limit is $500 and your balance is $250, your utilization is 50%.

We generally recommend keeping utilization below 20%. Lower is better. If possible, aim for 10% or less. This signals responsible credit behavior to lenders.

If you receive a low starting limit from the easiest unsecured credit card to get, make small purchases and pay them off quickly to keep your utilization ratio low.

3. Avoid Carrying a Balance if APR Is High

Many unsecured credit cards for bad credit have APRs above 25% variable, depending on the issuer and your credit profile. Carrying a balance at a high APR can become expensive quickly. If your card has a high APR, treat it as a credit-building tool rather than a borrowing tool. Use it for small recurring expenses and pay the full balance each month.

4. Keep the Account Open

Length of credit history affects your score. Even if you qualify for better cards later, keeping your first account open can strengthen your profile over time.

5. Limit New Applications

Each credit card application may result in a hard inquiry on your credit report. Too many inquiries in a short period can lower your score temporarily. Apply for one card at a time. Focus on managing that account well before seeking additional credit.

6. Monitor Your Credit Report Regularly

Check your credit report to confirm that your card issuer reports payments accurately. Monitoring your report allows you to track progress and dispute errors quickly if needed.

7. Increase Your Credit Limit Over Time

Some issuers automatically review your account after several months of on-time payments. A higher credit limit can lower your utilization ratio without increasing spending. If you start with the easiest unsecured credit card to get and demonstrate responsible use, you may qualify for a credit limit increase, which can further improve your score.

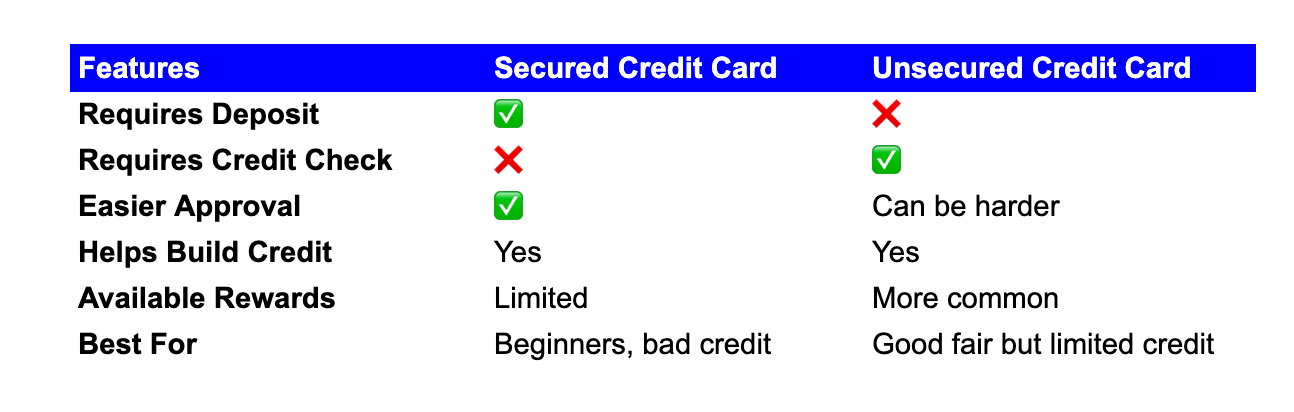

Secured Credit Card vs. Unsecured Credit Card

What Is the Easiest Credit Card to Get for Beginners?

Generally, the easiest unsecured credit card to get for beginners is one that considers alternative criteria (income history, bank account behavior) instead of relying on a strong credit score. Starter cards from fintech companies like Perpay, Zolve, Atlas, and Possible are tailored to be accessible to applicants with limited or no credit.

Below are 5 of the best cards that are often easier to get approved for.

The 5 Best Credit Cards Without a Credit Score or Credit Check

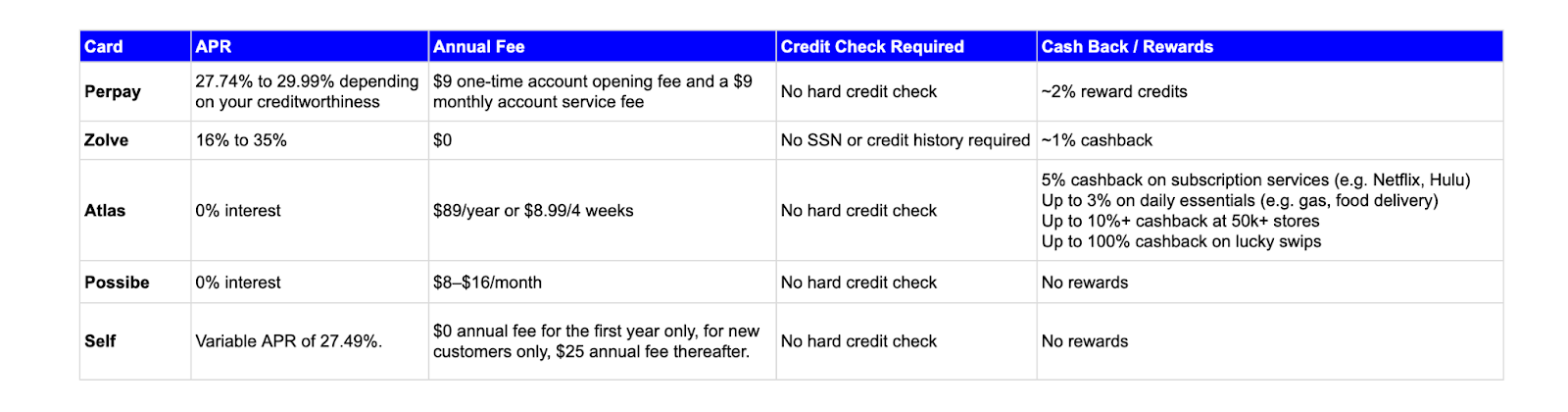

1. Perpay Credit Card

The Perpay Credit Card is an unsecured card that does not require a traditional security deposit or a hard credit check to apply. Instead, you link your direct paycheck to build financial trust with Perpay. Through this approach, Perpay can give you an unsecured credit card that’s backed by your own paycheck.

Why We Like It

Perpay is often easier to get than many traditional bank cards because it bypasses a formal credit report check and considers your income data. You can access up to $1,500 credit depending on income.

Pros:

- Easy approval

- Does not do a credit check

- Access up to $1,500 credit line

- Reports to major credit bureaus

- Earn rewards on payments

Cons:

- $9 one-time account opening fee and a $9 monthly account service fee (up to $108 annually)

- APR: 27.74% to 29.99% depending on your creditworthiness

Best For: People with limited or no credit history, but have stable monthly income and want to build credit this way

2. Zolve Classic Credit Card

The Zolve Credit Card is designed for newcomers to the U.S., such as international students or immigrants, and doesn’t require a Social Security Number or U.S. credit history to apply.

Why We Like It

Zolve makes it possible to build credit from day one in America, which is a rare feature among unsecured credit cards.

Pros:

- No SSN or U.S. credit history required

- Up to $10,000 credit limit

- 1% unlimited cashback

- Various cashback options

- Send and receive money internationally

- No foreign transaction fees

- $0 annual fee

- Reports to all three major bureaus

Cons:

- Fees for late payments if balance carried

- Variable APR: 16-35%

- Lack of APR and fee transparency on the website

Best For: Recent immigrants, international students, or anyone without a traditional credit profile.

3. Atlas Rewards Credit Card

Atlas Rewards Credit Card promotes itself as a card with high approval odds for people without credit history. It states that Atlas has over 4x higher approval rates than a traditional credit card and you can get an approval in two minutes. It provides 0% APR and generous cash back in popular spending categories.

Why We Like It

We picked Atlas because it blends credit building and cashback rewards. It reports payments to credit bureaus while offering up to 10% in cash back when shopping at 50,000+ stores like Target, Starbucks, and 5% on subscription products, including Netflix and Hulu. These perks set it apart from starter cards that offer no rewards.

Pros:

- High approval rates for limited credit

- Rewards on everyday spending

- 0% APR

- Card benefits such as cell phone protection, built-in auto rental coverage, extended warranty, and emergency travel assistance

Cons:

- Has an $89 annual fee or $8.99 monthly fee

Best For: People who want both building credit and earning rewards

4. Possible Card (coming soon)

The Possible Card promises a zero-interest card with transparent pricing. It offers access to $400 for $8 per month or an $800 credit limit for $16/month. Its zero-interest promise lets you choose from multiple payment options without incurring additional interest.

Why We Like It

Possible’s fixed cost model means you know exactly what you pay each month, and good behavior may help strengthen your credit. The card’s structure appeals to people who want to avoid traditional interest.

Pros:

- 0% APR

- Transparent pricing

- Flexible payment options with credit line up to $800 per month

Cons:

- To be invited for the card, it requires you to use their loan product.

- Not classic rewards

Best For: People who want cash flow-based approval and no interest.

5. Self Visa® Credit Card

Description

Self provides a more comprehensive credit-building system rather than just a standalone card. The Self Visa® Credit Card is one part of a larger ecosystem. With Self, users can build credit through three separate products: the Self Credit Builder Account, the Self Visa® Credit Card, and Self Rent Reporting. Because these products cover both installment and revolving credit, they can help improve credit mix, which may strengthen a credit profile over time.

Why We Like It

Self stands out because it combines a credit builder loan with a secured credit card. This dual structure allows users to build installment payment history and revolving credit history at the same time, which are two different credit scoring factors. Many starter cards only offer one type of credit reporting. That combination makes Self more comprehensive than many basic entry-level cards.

Pros:

- No credit checks. High approval rate.

- Reports to all three major credit bureaus

- Can build both installment and revolving credit history

- Low deposit requirement

- Strong brand recognition

Cons:

- 28.24% variable APR if balance is carried

- $25 annual fee after first year

Best For: People who want multiple credit-building products to build credit fast

Comparison of the 5 Best Credit Cards Without a Credit Score or Credit Check

Alternatives to Credit-Building Credit Cards

If you want options outside these unsecured credit cards, we recommend the below alternatives:

A credit-building product that helps you build credit through small purchases and payments reported to the bureaus without a traditional credit check.

Chime

While best known for banking, Chime’s Credit Builder Secured Card uses your Chime Checking balance as a deposit to create a credit line, with no credit check and no annual fee.

FAQ

1. What is the easiest unsecured credit card to get if I have bad credit?

Cards like Perpay and Atlas are among the easiest because they use alternative underwriting or bank data instead of strict credit score checks.

2. Can I get an unsecured credit card with no credit history?

Yes. Some fintech cards, like Zolve and certain starter cards, allow you to apply without a credit history.

3. Does the easiest unsecured credit card to get help build credit?

Yes, as long as the card reports your payments to major credit bureaus, on-time use will help build your credit.

4. Do unsecured cards require a security deposit?

No. That’s the defining feature. Unsecured cards do not require a security deposit but may have fees.

5. How soon can I build credit with an unsecured credit card?

Credit bureaus usually update reports monthly, so consistent on-time payments over a few months can begin to show positive changes.

Final Thoughts

The easiest unsecured credit card to get depends on your personal situation — if you have no credit history, cards like Zolve and Atlas may be accessible, while tools like Perpay and Possible offer alternative underwriting that doesn’t hinge on traditional credit scores. Always pay responsibly, keep utilization low, and remember that building credit is a marathon, not a sprint.

Start Building Credit with Firstcard

- Build credit faster

- No credit check or hard inquiry

- Accepts international students, immigrants and foreigners without SSN

- 0% APR

- Get up to 1% unlimited cashback

- Get up to 4.00% APY

Credit building

for all

.webp)

.png)

.svg)